Two months ago, Scott Bessent, Stephen Miran and Convertingal Macroeconomic Analysts All Agreed on One Point: An Increase in tariffs Shield Raise the Value of the Dollar.

Cea Chair Miran also Expected A Rise in the Dollar. Some of the Ideas in his (In) Famous Paper Seem to Have Been Intended to Address The Difficulties a Strong Dollaar Welf Generate for A Policy that Aimed to Reduce the Trade Deficit.

Convetional Economic Analysts Pointed to the “Lerner” Symmetry Condition, Which Argues that a Tax on Imports is Effectively a Tax on ExportsEven Absent Foreign Retaliation. Less Imports Means that Foreign Counties Have Fewer Dollars to Spend on Exports (this Analysis Holds with Unparanced Trade and Capital Inflows if the tariffs have no impact on Capital Flows and Thus Demand for Dollars from the Financial Account).

Wall Street -end the city -initially Agreed with this Analysis.

Follow the Money

Brad Setser Tracks Cross-Border Flows, with a bit of macroconomics Thrown in.

Going “Long” The Dollar (Betting on Appness) was a standard “Trump” Trade IMMEDIATE after Trump’s Electional. Investors Bid Up the Dollar in Anctification of Tax Cuts that would make us equiges more attaculting –or Beautiful them Exerced that Tarifs Promised During During During Durling The Campaign Wood Reduce the Supply of Dollars by Bringing Download the Trade Deficit.

But this Trump Trade DIDNNT WORK. Tarifs Surprised to the Upside, Yet the Dollar Has Slumped. It is now down around 10 Percent Against Some now Believe that the Dollaar Hit A Long-TURINING POINT.

More on:

Economics

International Finance

Currence Reserves

Trade

International Economic Policy

So, Why did’s tariffs push up the dollar? I can think of Five Theities:

1. The Tarifs AR AR A Tax Hike, and Fiscal Consolidation is Bad for the Dollar.

If the US SIMPLY RAISED ReveNues Through A Consumption Tax, No One Wald Have Extended the Dollar to Rally. The 10 Percent “Base” TARIFF On Most Trade (Oil is Exclouded, as usmca-Compleant Trade with north Americana) has some characterismics of a consumption Tax. The gigantic Current Tariffs on China Won’t Generate any Really Revenue in the Long Run, But It’s Unreasonable to Expect that a 10 Percent Tarif on, Say 7 Percent of Us Trade Will Generate A Modest Long-TERM Revenue Stream. The 25 Percent Security Tariffs on Steel, Autos, Pharmaceuticals and selectingors –collectively Around 3% of GDP Even without counting Imports –shoul GENERATE A Bit Of Revenue in The Short Run. Absent any Offsetting Tax Cuts and Even after considering The Resulting Expected Slodown Has LED The Market to Expecting that Fed will Cut

2.

Many Analysts How Expect A Significant Download in the US In Q2 and Q3. That should be Bad for equits, and the long -ru impct of the tariffs on center stores is unlikely to be positive. Apple, for Example, Now Face A 20 Percent Tarif on Phones Imported from China (From the “Fentanyl” National Security Case) and a 10 Percent Tarif on Phones Imported from India, with the Risk Of more tariffs. Those Phones for Arrive at Us Customs at a Price of $ 400 To $ 550 (The Retail PRICE is Obvivally High, but Apple Applies Its Markup on Us Sales after the Phones Cross the Border). That is a $ 40- $ 110 Tax Per iPhone. Some of that will be passed on to consumers, but some will be absorbed out of apple’s margins. Apple’s challenge is modest IEPA/Fentanyl Tariff. DMAND for us assets wasnt, in faccant in the Face of the Tarifs, as the Tarifs Have an Impact on the Value of Certain us assets.

3. China Held the Line.

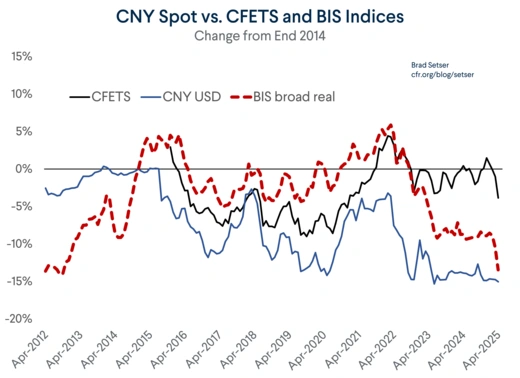

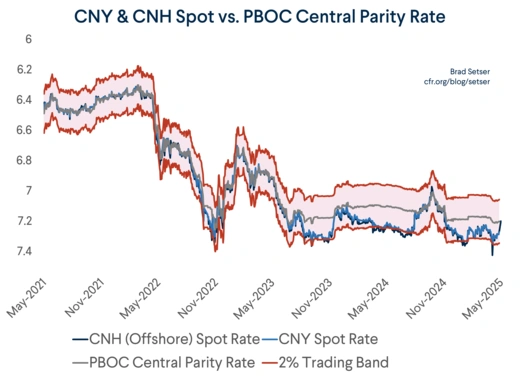

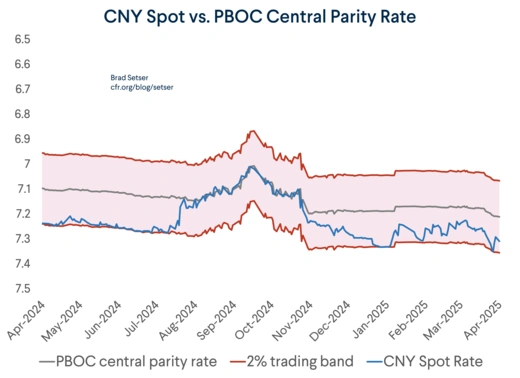

Trump’s First Term Trade Was Was Largely Directed at China, and China Responded to Tariffs by Letting the Yuan Slide.That was a Relatively Easy Pressure Valve to Release back in 2018 and 2019, as the Yuan Started the Trade War At A Relatively Elevated Value (6.4 to the Dollar Or so) Yuan Fall To 7 or Even A Bit Beyond. A Weak Yuan in Turn LED Other Asian Currencies to Fall in Sympathy.

But with the yuan already at Long-TERM LOWS (Around 7.3) China Has Been Rellructant to Allow the Yuan to MOVE-end Risk Disrupting

China also may now think that is better to make sure that us imperrtrs Don’t get a disscount on chinese goods … or simply be happy to Allow the Current Weakness in the Dollar to Pull the Trade-WEIGHTED RENMINBI Download. What China’s Motive, The Absence of a Political Decision by China to Put The Yuan Back in Play Help Limit Dollaar Weakness.

4.

The Initial Trump Trade Assumed, More Or Less, that American Trading Partners Wouldn’t Change their Policies in Ways that Made Their Currencies More Attractive. That turned out to be Wrong. GERMANY DROPDET ITS POICY OF Self-Imposed Austerity– ALLOWED More Borrowing for Both Investment in Its Security and Investment in Its Infrastructure. Sweden Too. Even The Irish Are Reportedly Now Ready to Spend a Bit More on Defense. Fiscal Easing in Europe’s Prevringly Frogal North Should Hel Support Euroan Growth –and also inclly of the supply of the Most Desired Euro-Denomiadated Financial Asset (Supply Of “Bunds”-Long-TERM BONDS ISSUED by GERMANY’s Federal Goovernment –Previviously Fell Well-Short of Global DEMAND For Euro-duINMENMENMENMEGN ExchandES Reserves, Let Alone Global Demand for Eurobean Safe Assets from Both Public and Private Sources).

5.

Trump (Perhaps Surprisingly) Wants the Dolar to Remain The World’s Reserve Currency. Ineduted a bit of A RISK Premium Into Dollar Assets (Or a Bigger Term Premium Into US Treasury Bonds). A us that trades less makes Holding an asset that is accented by the dollar party network work a bit less (Even if the dollaar Can Still be used to setting the Payments Between Thred Parties). And if Us Allies Fear that They Might Be COERCED by An “American First” Pressing to Pay for the Security Provided by ALLIANCE with the Us Through A Tax on Their Us Us Holdings, Well, that makes Dollar Claims on the US Bit Riskier.

Additionlly, some big state instertains Potentially Face Pressure Not to Invest quite so much in the use if the use is the three Institutions. If the use is going to restect canada’s independence, Shuld Canadian Public Pensions Be so Investd in the US?? If the use it won to receive danish Soovereignty, Should Danish Pensions and Reserves Be Invested in Dollars? Will Norway (Whiche Has a Big Sooven Wealth Fund) and sweden (whom has lot punch pensfonds) Stand by their scandinavian Neighbor? There are loots of stockpiled legacy surpluses in Europe as well as in asia.

There is, of course, the Question of what a china that no longer trades with the US will control to Keep 55 Percent of Its Formal Reserves (See Safe’s 2023 Annual Report) And a Much Highher Share of the Foreign Currency Asset Base of Its State Banks in Dollars.

In a Sense, The Dollar’s Recent Weakness Is Over-Determined.

There is also the simple facing that of the dollaar was Exceptionally Strong and Thus The Odds Were that is Welf Fall at Some Point. The Flow Equilibruum Around the Dollar request Ever Increasing Inflows from the Rest of the World at Ever More Inflate Vals of the Dollar and Us Equits – The So Called us Exceptionalism Trade.

And that trade was starting to show its age ever before Election of Donald Trump (See James Aitkeen).

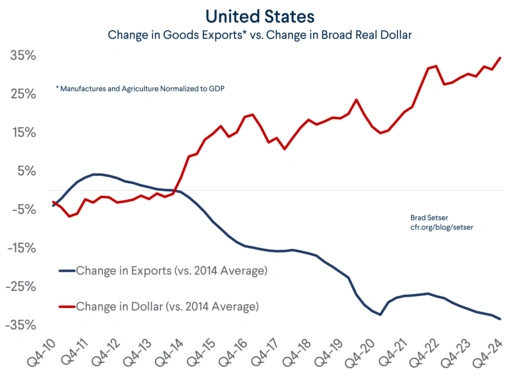

The 2023-24 Dollaar was at a level that is imipied an ever-shrinking US Export Base.

It was also at a level that is imipied an ever-groping trade deficit.

Dollaar Strength Was Even Weight on the Offshore Income Streams Generated by America’s World League Digital Platform Companes – IP Exports and FDI Profits Were Falling As A shary of Us GDP.

But the Dollar’s Download.

What’s more, Even with the recent Slide, the Dolar Is Still Quite Strong by Almost All Measors.

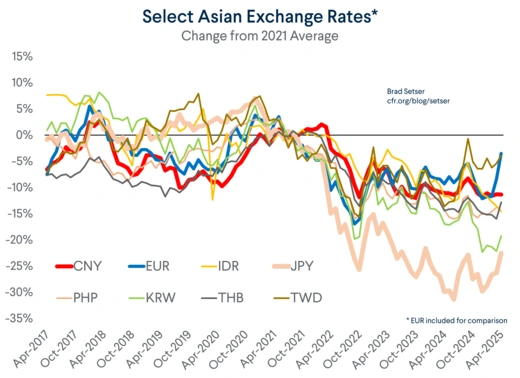

CNY 7.2, KRW 1400, JPY 140; Anyone Who Remembers the Dolar’s Levels Against the Big Asian Currencies Five Years ago Wold Say that these are award “Weak” levels for the dollar (Notwithstanding the Somewhat Exaggerned Claims that Float Around About the End of the Dollar’s Global Reign).

In Some Sense, Though, The Main Constrain on Dollar Stregth is that the Most Trade-EXPOSED COUNTRIES in asia are themes Facing A Big Shock, and Unlike EUROPE, They Don’t seemitted To a Big Fiscal Resporese.

They Thus Face A Bit of a Dilemma if their Currencies Rise from the Reportability of Past Investments and Hedging Flows Even as GLOBAL Trade Slos.

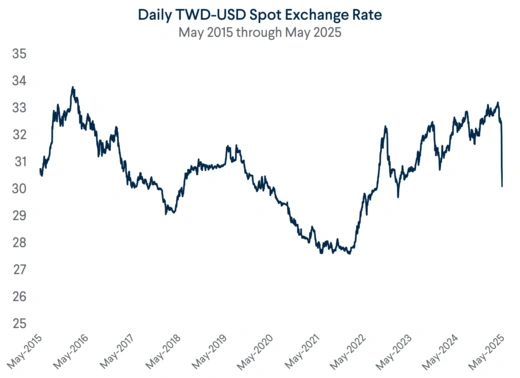

Taiwan is a great card in question. Private Taiwanese Investors Have Built Up a Massive Holdings of Dollar Assets (Mostly Bonds, and Heavily Corporaate Bonds) and they generally having’t Hedged that Exposure (Hedging Has Been Expective, and it is different for the world as a whole to be Hedged Against the Dollar When The Us Funds Its External Deficit in Dollars).

And thus Hedging Flows from Over-EXNDED LIFE Insurance Companies Could Put upward put on the Taiwan Dollaar, as on Monday. The Real Question JOW MUCH DOLLAR Weakness Is Too Much for Taiwan’s Center Bank (The Secret Bank of China) and how will the United Stats Treasury Respond if Taiwan English In Large Scale, One Sided Interversion in the Foreign Exchang Market to Curb Pressure on the Taiwan Dollar to Apprecital, and in the procese keep the dollar artificially strang?

{kind=link}